Singapore REITs have come under intense pressure in recent months due to a rising interest rate environment, persistently high inflation, and rising geopolitical tensions. It doesn't make things rosier with the latest FOMC meeting. During the last FOMC meeting, on September 19-20, 2023, the Fed held rates steady at 5.25-5.50%, taking a pause from an aggressive rate-hiking campaign that began in March 2022 to fight rising inflation. The Fed also signalled that it could continue to raise rates at least one more time this year since most officials view this as necessary to bring inflation down to the 2% target over time.

REITs are typically highly leveraged, meaning they have a lot of debt. This makes them more susceptible to rising interest rates, as they have to pay more interest on their borrowings. At the same time, REITs have to compete with fixed-income investments, such as T-bills, which are now offering more attractive payouts. For example, the latest 6-month T-bills are paying 4.07% p.a., while S-REITs have an average dividend yield of 7.5% p.a.

In addition, REITs are facing challenges within their individual segments. Office REITs are seeing a decline in demand as more people work from home. Retail REITs are competing with the growing popularity of e-commerce. REITs across all sectors are facing higher operational costs due to inflation.

As a result of these headwinds, S-REITs have seen their share prices fall and their dividend yields rise. This suggests that investors are becoming more cautious about the sector.

How S-REITs Have Performed for Q3 2023

Looking at the chart below, we can see that the overall S-REIT market has fallen nearly 7.68% for Q3 2023.

Source : SGX - iEdge S-REIT Index

The Straits Times Index (STI), made up of the 30 strongest stocks in Singapore, literally stayed flat and returned a positive of about 0.32%, for Q3 2023.

Source : SGX - Straits Time Index

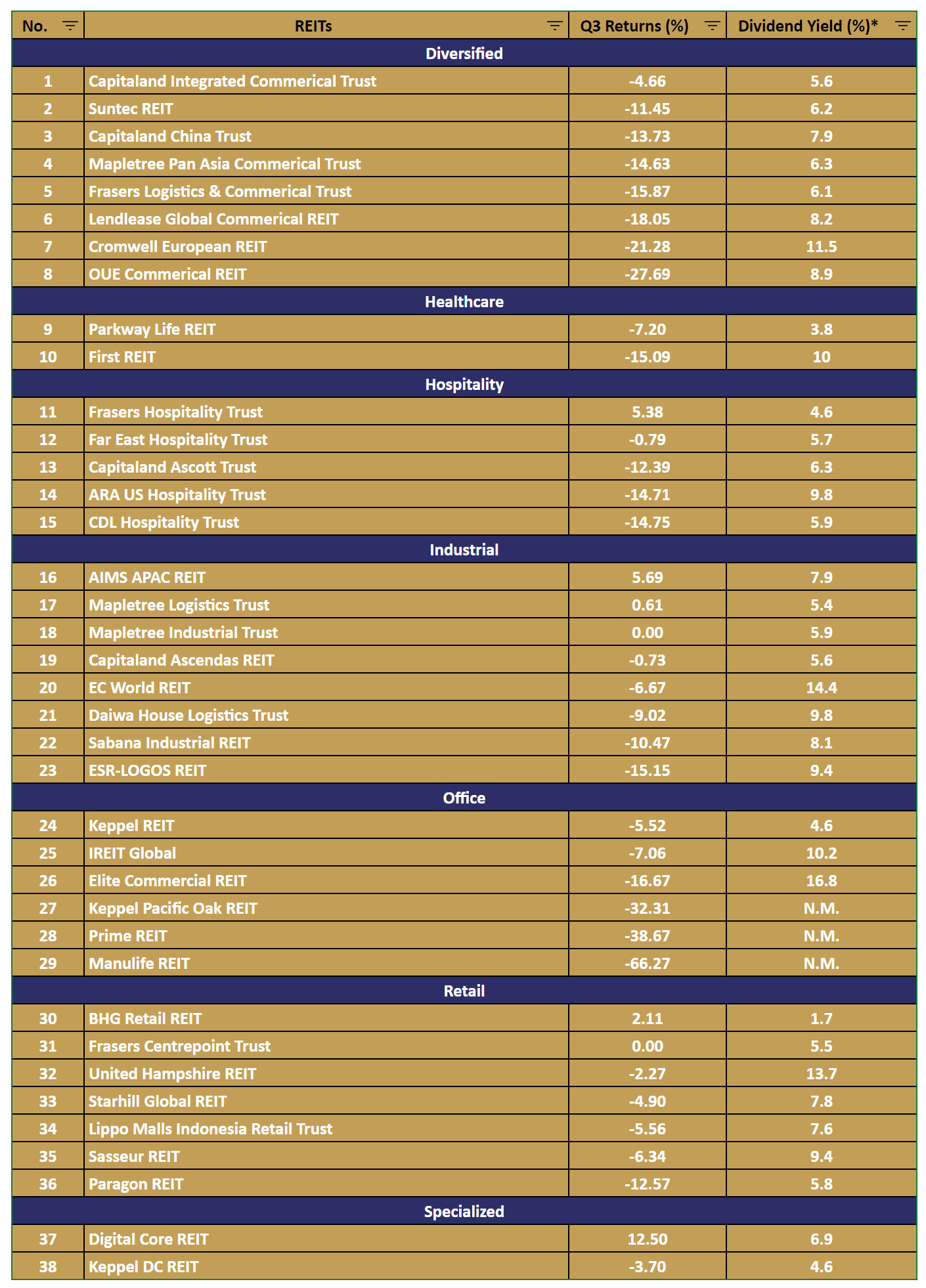

How Individual S-REITs Have Performed for Q3 2023

Source : SGX

Dividend Yield derived from SGX Chartbook - SREITs & Property Trusts Chartbook – 18 September 2023

Best Performer S-REIT for Q3 2023 - Digital Core REIT (12.5%)

Digital Core REIT's share price fell sharply in March 2023 due to fears that the collapse of Silicon Valley Bank and the troubles at First Republic Bank could spread to other financial institutions, including those in the US and Canada. Investors were concerned that Digital Core REIT may have funds parked in these financial institutions, or that its tenants may have banking relationships with them.

Digital Core REIT's CEO, John Stewart, publicly assured investors that it had no customer or banking relationship with the beleaguered banks and that three-quarters of its annualized revenue was of investment grade or the equivalent. However, investor sentiment remained jittery for several months following the collapse of Silicon Valley Bank and First Republic Bank.

Then again in early June 2023, Digital Core REIT's second-largest tenant, Cyxtera Technologies Inc., filed for Chapter 11 bankruptcy. Cyxtera represents 22.4% of Digital Core REIT's annualized rental revenue, so the news was initially concerning for investors.

However, there were some silver linings. A Chapter 11 filing meant that Cyxtera could now decide which leases it wished to accept or reject. This gave Digital Core REIT some much-needed flexibility. Additionally, the REIT's CEO, Stewart, publicly assured investors that Digital Core REIT had no customer or banking relationship with Cyxtera and that the REIT was well-positioned to weather the storm.

As a result of these silver linings, Digital Core REIT's share price rebounded sharply after the initial sell-off. Investors were confident that the REIT would be able to manage through the Cyxtera bankruptcy and continue to generate attractive returns.

Since then, Cyxtera has resumed paying its rent for July and Digital Core REIT has been able to claim June's rent through the bankruptcy process. Additionally, there have been reports that multiple parties are interested in acquiring Cyxtera's assets, including Digital Core REIT's sponsor, Digital Realty Trust.

Recently, it was also announced that Digital Core REIT was included in the FTSE EPRA Nareit Global Developed Index on 15 September, which is designed to track the performance of listed property companies and REITs around the world. This inclusion is expected to enhance the REIT's trading liquidity and attract new capital inflows from global index funds.

Digital Core REIT's CEO, John Stewart, believes that the index inclusion will be a positive development for the REIT. "We are delighted to be included in this global REIT index," he said. "This inclusion is a testament to the quality of our portfolio and our strong financial performance."

Investor sentiment on Digital Core REIT has undoubtedly improved over the past few months. On the positive side, the data centre market could benefit from increased data storage demand with the AI boom.

Worst Performer S-REIT for Q3 2023 - Manulife REIT (-66.27%)

Manulife REIT announced that it would not pay out any distributions for the first half of 2023 in a press release on 14 Aug 2023. This is a highly unusual move for a REIT, as most REITs aim to pay out consistent and dependable distributions to their unitholders by owning and managing a portfolio of properties that generate rental income.

There are two key reasons for MUST's decision to suspend distributions:

- Breach of financial covenant: MUST has breached a financial covenant in its financing documents. This covenant likely relates to a debt-to-equity ratio or other measure of financial health.

- Uncertainty about the ability to meet liabilities: The REIT manager cannot confirm that MUST can meet its liabilities if a distribution is paid. This means that the REIT may not have enough cash to pay its debts and other obligations if it pays out a distribution to its shareholders.

The suspension of distributions is a negative development for shareholders. It means that they will not receive any income from their investment in the REIT for the first half of 2023. It also raises concerns about the financial health of the REIT.

Worrying signs already began in 2020 when the REIT suffered three consecutive years of declining DPU.

| Year | DPU (US$) | YOY % |

|---|---|---|

| 2019 | 0.0596 | +7.0% |

| 2020 | 0.0564 | -5.4% |

| 2021 | 0.0533 | -5.5% |

| 2022 | 0.0475 | -10.9% |

The decline in DPU is due to a number of factors, including:

- Provisions made for expected credit losses from retail and F&B tenants

- Higher rental abatements and lower rental income stemming from higher vacancies as COVID-19 hit

- Higher inflation and surging interest rates buffeted the REIT and caused its finance costs to jump by 16.4% year-on-year

- An increase in units arising from a private placement

The trigger for the financial covenant breach was a further decline in its portfolio valuation for 1H 2023. The US office REIT's valuation slid 14.6% from US$1.91 billion as of 31 December 2022 to US$1.63 billion as of 30 June 2023. This coincided with a steep fall in overall US office valuations of 18.4% in the second quarter of 2023, as measured by the NCREIF Property Index.

The US office market is facing a number of challenges, including rising interest rates, higher vacancies, and lower valuations. These challenges are likely to hinder the REIT's recovery from its financial difficulties.