Are investors focusing too much on headline DPU when evaluating Singapore REITs? Michelle Martin examines why the familiar distribution-per-unit number may not tell the full story.

In this episode of Money and Me, we explore whether investors should shift their focus from the quantity of distributions to the quality and sustainability behind them.

REIT specialist and Wealth Advisory Director Kenny Loh introduces a new framework - the Management Efficiency Index (MEI) - meant to help investors evaluate how effectively REIT managers generate and protect long-term income.

The conversation also unpacks the risks behind 100% payout strategies, accounting optic moves, and the impact of management fees paid in units.

With AGM season approaching, Kenny shares the key questions retail investors should ask management teams to better understand the resilience of distributions.

Any investor heading to a REIT AGM would benefit from knowing the right questions to ask to dive beyond the numbers to get at management "sweat equity".

You can listen to the podcast over here.

Question by Michelle Martin

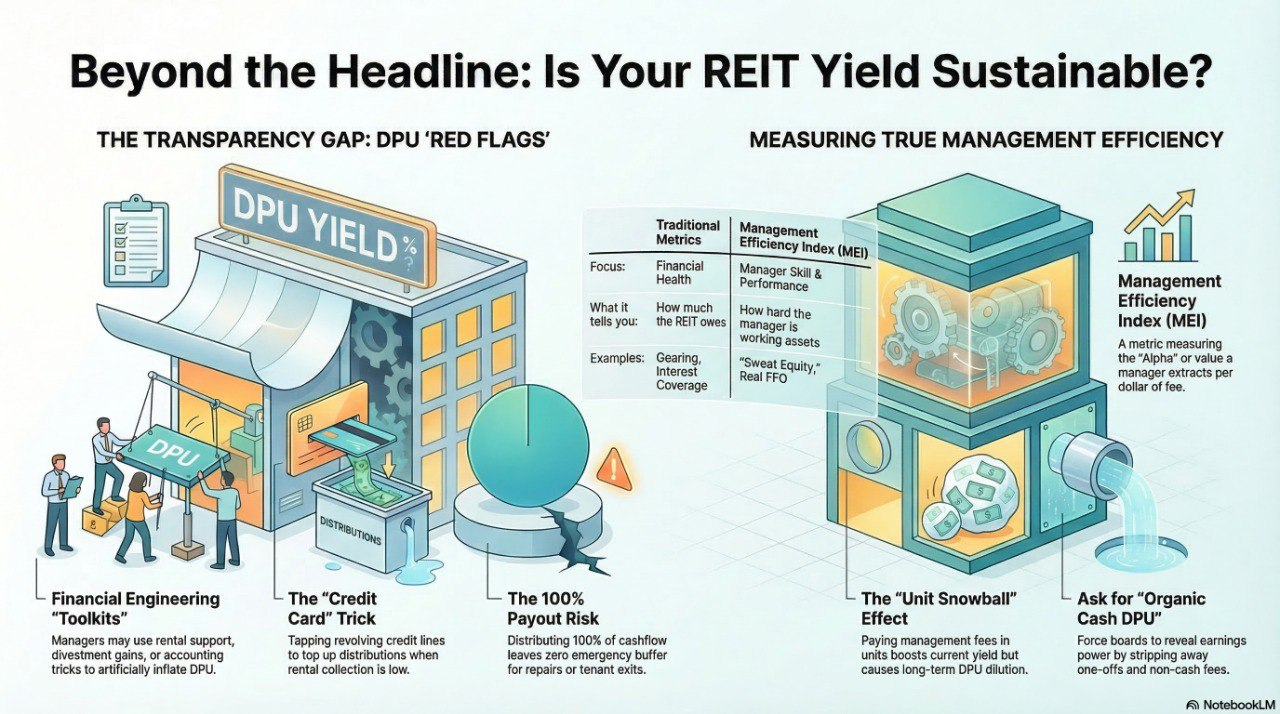

Many investors focus solely on the headline DPU, but you’ve highlighted a "Transparency Gap" in statutory statements. What are some of the specific items that can mask a REIT's core rental cashflow?

Answer by Kenny Loh

The "Transparency Gap" & Masking Core Cashflow

The headline DPU is a bit like a 'Gross Salary' vs. 'Take-Home Pay.' The big number on the contract looks amazing, but after you strip away the one-off bonuses and accounting tricks, the actual 'spendable' cash can be a lot smaller. We’re warning investors not to fall in love with the big number before checking what’s actually left in the bank.

Many investors treat Distributable Income as synonymous with "profit," but it’s actually a highly adjusted figure. Specific items that mask core rental health include:

- Rental Support/Guarantees: These are top-ups from sponsors that artificially inflate income when a building is empty or underperforming.

- One-off Divestment Gains: Using "capital gains" to pad the DPU when organic rental growth is flat.

- Amortization of Lease Incentives: This is the Accounting 'magic' that hides the fact that a tenant got six months of free rent.

Question by Michelle Martin

When we look at DPU "manipulation" or optics, how do management teams typically bridge the gap between actual operational earnings and the distributions paid out to unitholders?

Answer by Kenny Loh

Bridging the Gap: Optics vs. Earnings

Management teams aren't necessarily 'faking' it, but they are using some very creative financial engineering to bridge the gap." Management teams have a "toolkit" to maintain DPU optics even when the properties aren't delivering.

The most common methods are:

- Management Fees in Units: Instead of paying the manager in cash, the REIT issues new units. This "saves" cash to pay unitholders but leads to long-term dilution.

- Capital Distributions: Returning a portion of the original investment (capital) back to unitholders, which is essentially giving you back your own money to keep the yield looking high. It’s like taking $10 out of your left pocket to put $10 in your right and saying you've made a profit.

- Swiping the Revolving Credit Line (Credit Card Trick): "When rent collection is slow or a major tenant leaves, a manager might tap into their Revolving Credit Facility (RCF)—essentially the REIT’s corporate credit card. They draw down debt to top up the distribution pot so that unitholders don't see a dip in their quarterly check. On the surface, the DPU looks stable and 'safe,' but in reality, that payout wasn't earned from tenants; it was borrowed from a bank." This is something like, you paid 5% or 6% interest to the bank so the REIT can give you a 6% yield. It’s a zero-sum game that actually erodes the Net Asset Value (NAV) and reduced the debt ceiling over time.

The 'Why' (The Painkiller): "Why do they do it? Because the market is brutal toward DPU cuts. A 2% drop in DPU can trigger a 10% sell-off in the stock price. The manager uses the credit line as a financial painkiller to mask the symptoms of a weak portfolio, hoping that 'tomorrow' will be better so they can pay the bank back. But as we know, if you keep using one credit card to pay another, eventually the interest catches up with you."

How can an investor spot this?"

Go to the Statement of Cash Flows. If the 'Net Cash from Operating Activities' is consistently lower than the 'Total Distributions Paid,' you know they are borrowing from Peter to pay Paul. It’s a huge red flag for the sustainability of that yield.

Question by Michelle Martin

You’ve raised concerns about the "100% Payout Risk." Why might distributing every cent of operational cashflow be a red flag rather than a sign of strength?

Answer by Kenny Loh

The "100% Payout Risk"

While a 100% payout ratio looks generous, it can be a red flag. It means the REIT has zero margin for error.

- Michelle, let’s look at this through the lens of a personal finance. Distributing 100% of cashflow is like a person spending every single cent of their paycheck the moment it hits their bank account. They have zero emergency funds. Now, ask yourself: What happens to that person if they suddenly lose their job, or if a family member has an unexpected medical emergency? They have no buffer. They’re forced to take on high-interest debt or sell their belongings just to survive.

- It’s the same with a REIT. If they pay out 100%, they have no 'rainy day fund' for a major roof repair or a sudden tenant exit. They’re forced to either borrow more at today’s high rates or ask unitholders for more cash through a rights issue. To me, that’s not a sign of a 'generous' manager; it’s a sign of a manager living paycheck-to-paycheck.

Question by Michelle Martin

How should investors interpret the use of management fees paid in units rather than cash, and how does this impact the long-term DPU trajectory?

Answer by Kenny Loh

Management Fees in Units: The Long-term Impact

Think of this as a 'Buy Now, Pay Later' scheme for DPU."

- The Impact: Short term it props up the yield today, but it creates a 'Unit Snowball” in the long term as it increases the total unit base. More units mean the next year’s earnings have to be split among more people. Unless the property performs like a rockstar, the DPU will eventually face downward pressure because the "pie" is being sliced into more and more pieces every year.

Question by Michelle Martin

Regarding newly listed entities like UI Boustead REIT, what specific efficiency signals should investors look for in the early stages of a REIT’s life cycle?

Answer by Kenny Loh

Early Efficiency Signals: UI Boustead REIT & New Listings

For a new listing, don't just fall in love with the 'IPO Yield.

Efficiency Signals:

- Look for a high NPI Margin (Net Property Income). If the manager can’t run a brand-new portfolio efficiently now, they certainly won't when the buildings start to age

- Portfolio Occupancy vs. Market Average: Is the initial high yield propped up by a single "trophy" tenant, or is there a diversified, high-quality base?

- Lease Decay: How the REITs address the lease decay, which impact NAV due to short land lease tenure for Industrial property in Singapore.

- Expense Ratio: Are administrative costs bloated relative to the size of the portfolio? The large scale of economy should bring the unit admin cost down but not the other way.

Question by Michelle Martin

How does the Management Efficiency Index (MEI) differ from traditional metrics like Gearing or Interest Coverage Ratio when assessing a manager's performance?

Answer by Kenny Loh

Management Efficiency Index (MEI) vs. Traditional Metrics

Traditional metrics like Gearing or Interest Coverage Ratio tell you about financial health, but the MEI tells you about manager skill and performance.

- MEI was created by my REITsavvy team to measure the "Alpha" or extra value a manager extracts from the assets per dollar of fee they take.

- In the US, investors don’t just look at dividends; they obsess over FFO (Funds From Operations). Think of FFO as the 'True North' of a REIT’s performance. It’s a metric that ignores the accounting 'smoke and mirrors' and focuses purely on the cash generated by the properties themselves.

- The Management Efficiency Index (MEI) brings that same discipline here. We believe a manager's primary job is to be a great landlord, not a financial engineer. While traditional metrics like Gearing tell you how much the REIT owes, the MEI tells you how well the manager is working the assets. It filters out the 'cheap debt' or 'top-up' tricks and asks: 'If we strip away the fancy financing, how much real value is this manager actually squeezing out of these buildings?' It’s about measuring the 'sweat equity' of the manager, not just their ability to sign a loan document."

Question by Michelle Martin

In an environment of higher-for-longer interest rates, how can an investor distinguish between a manager who is "entitled" to fees and one who is actively creating value?

Answer by Kenny Loh

Distinguishing "Value-Add" from "Entitlement"

When interest rates stay high, the 'lazy' managers get exposed. The 'entitled' ones keep collecting their base fees while the share price tanking is 'not their fault’.

- The Value Creator: They take the pain with you. They hedge aggressively, they find ways to cut utility costs, and they might even pivot to cash fees to stop the unit dilution. They act like owners, not just employees.

Question by Michelle Martin

For those heading into AGM season, what is the one question every retail investor should ask the board regarding the sustainability of their distributions?

Answer by Kenny Loh

The One Question for AGM Season

If you only ask one thing, make it this:

"Excluding one-off capital distributions and management fees paid in units, what is your 'Organic Cash DPU' and is it sufficient to cover the current payout, and show the trend Year on Year".

This forces the board to strip away the "optics" and reveal the true earnings power of the properties. I urge all investors to ask this question in the AGM. Invite them to listen to this podcast Money&Me with Michelle Martin for a more direct and transparent reply.

Question by Michelle Martin

Looking ahead, do you expect more S-REITs to shift their reporting focus toward these efficiency metrics, or will the market remain anchored to the headline DPU?

Answer by Kenny Loh

Future Outlook: Efficiency vs. Headline DPU

The current market is still addicted to the 'headline DPU'—it’s the 'fast food' of metrics. It’s quick, it’s easy to digest, but it doesn't tell you anything about the long-term health of the REIT.

As we move past the era of 'cheap money,' the big institutional players are already switching to an 'organic' diet. They aren't just asking 'What is the yield?' They’re asking: 'How hard did the manager have to work to get this yield?'

As an educator in this space, my mission is to move the needle on transparency. I want to see REIT managers move away from financial engineering and get back to their core role as disciplined landlords. We need to start measuring things like the Management Efficiency Index (MEI) or Real FFO because, in business, what gets measured gets done. If we focus on real cash flow and property value creation rather than just the decimal point on a dividend, we’ll build a much more resilient REIT market for everyone